JBY announces 1.37M ounces of gold maiden JORC resource - more drilling starting in the coming weeks… and it’s in the USA

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,979,167 JBY shares and the Company’s staff own 33,334 JBY shares at the time of publishing this article. The Company has been engaged by JBY to share our commentary on the progress of our Investment in JBY over time.

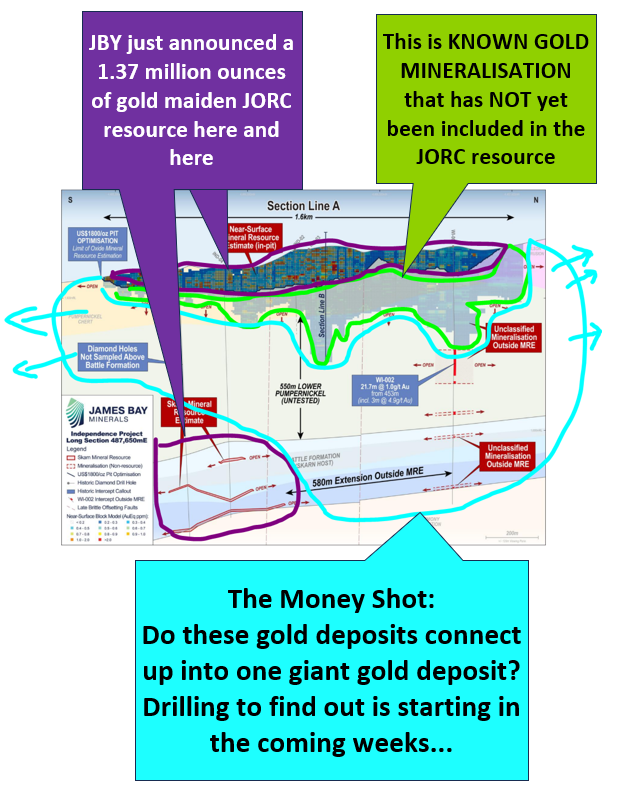

James Bay Minerals (ASX: JBY) just delivered a maiden JORC resource of ~1.37M ounces of gold.

With drilling commencing in a few weeks to start testing a theory that could multiply its size...

JBY’s project is in Nevada, USA.

The USA is currently our favourite place for gold projects because we think something big is about to happen between the USA and gold.

The USA is buying and importing record amounts of physical gold in recent months.

The gold price keeps hitting new all time highs and feels like it wants to keep running.

Two weeks ago we wrote about the unusually high amount of high profile US public figures suddenly talking about gold...

Donald Trump, Elon Musk and various US Senators have started talking about gold over the last 20 days (read it here)

One week ago we noted that the mainstream mentions of gold were increasing, with political commentator Tucker Carlson talking about the importance of gold for 90 minutes (read it here)

Even the most followed podcaster in the world, Joe Rogan is talking about gold for some reason.

Why?

Reading into the noise, it feels like something big is about to happen with gold, and the USA is getting primed for it.

For us as Investors, we think gold in the ground in the USA could be about to get more valuable.

JBY now has a JORC “in the ground” resource estimate of 1.37M ounces of gold.

This is an upgrade of ~200k ounces from its previous non JORC resource estimate.

(an upgrade in size was an unexpected positive surprise for us)

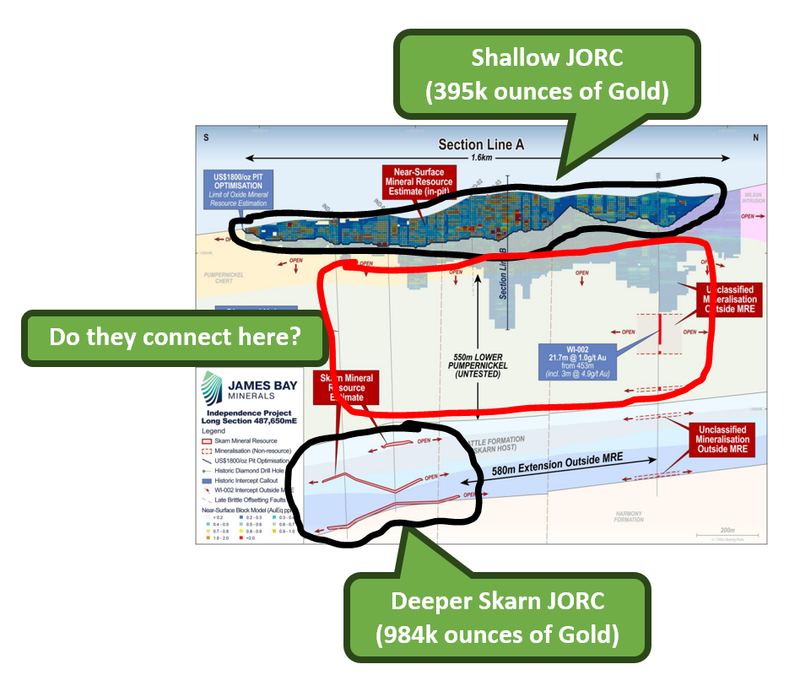

~395k ounces of that is from shallow near surface mineralisation.

The other ~984k ounces is from a deeper (much higher grade) section of the project where average grades are ~6.67g/t.

And it's in the USA - our current favourite place for precious metals projects because, as we said above - it's where we think something big is about to happen in the gold space.

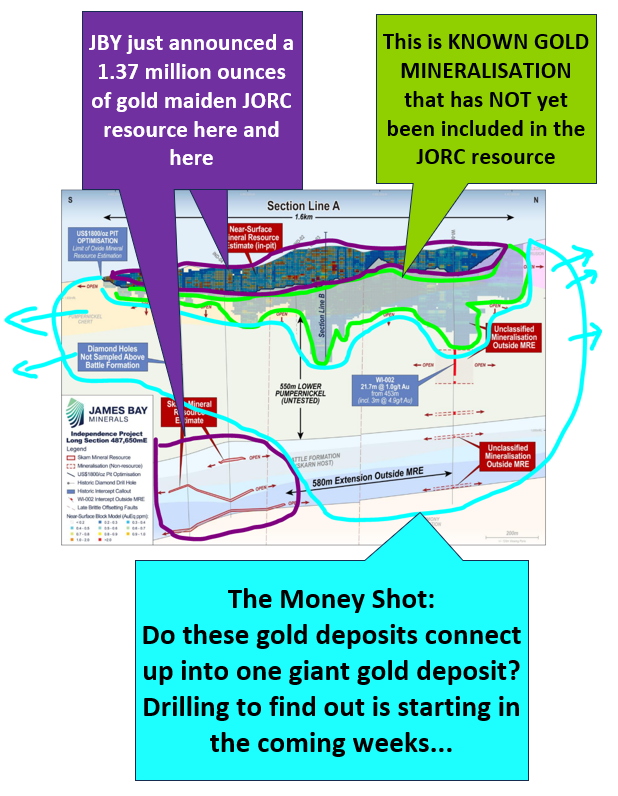

The question JBY now needs to answer is do its separate, known gold deposits join up into one giant gold deposit?

Drilling is the only way to find out...

And JBY is starting drilling in the coming weeks.

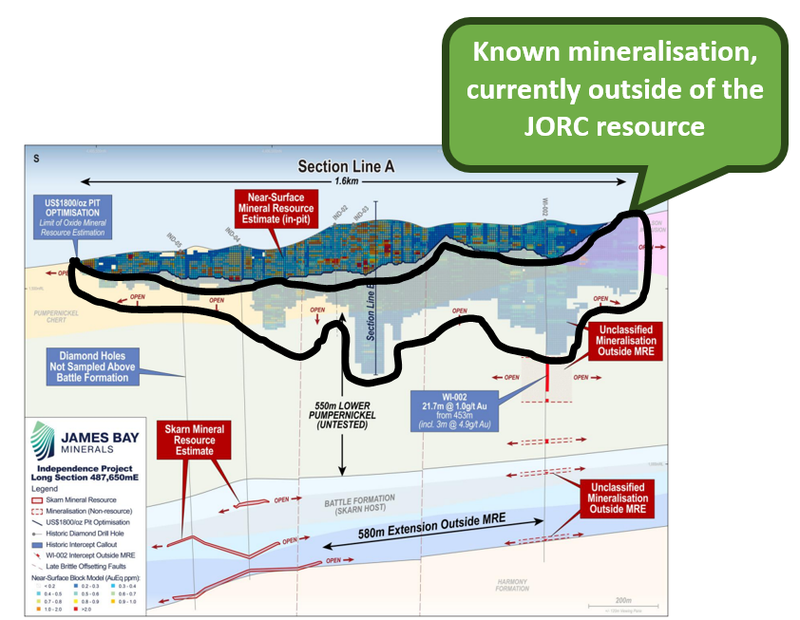

There is still a lot of mineralisation sitting outside of today’s resource estimate...

The resource, as it stands today is already very big, but we think there are three ways JBY could add to its resource in a meaningful way:

- By building in the known mineralisation outside of the current resource model.

- By drilling out the area between the shallow and deep mineralisation

- By drilling extensions to the current JORC resource.

That’s where the next round of drilling comes into play.

JBY had ~$7.3M cash in the bank at 31 December 2024 and will be drilling this quarter.

(Its last capital raise was in December when it raised $6M at 65c, above the current market price)

We think JBY has a reasonable amount of cash runway to deliver exploration upside results in a red-hot gold market.

Ultimately, JBY’s exploration drilling will be aiming to multiply the current resource, and all going well, deliver a sustained share price re-rate.

Especially if the gold price keeps going up and to the right like it has been in the 5 year gold chart:

So... how can JBY multiply its current resource?

1. Build in known mineralisation outside resource model

First, the known gold mineralisation that sits outside of the current resource model - none of this was factored into today’s 1.37 million ounces.

With some drilling, there is a chance JBY gets this into its resource calculations come time for resource upgrades.

2. Connecting the deeper gold to the shallower gold

The second idea is a bit more conceptual, but there seems to be some precedent for it.

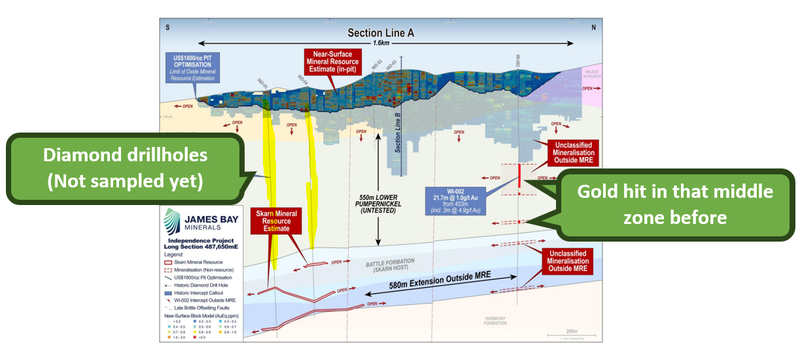

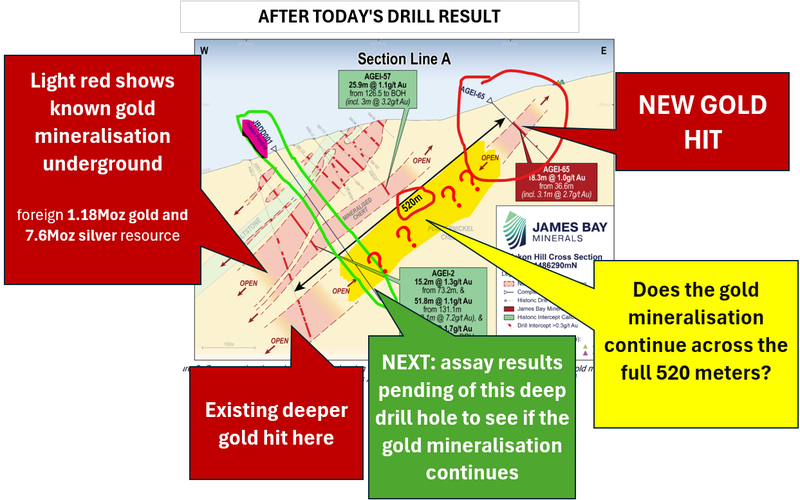

The idea is that the shallow near surface gold extends at depth and connects to the higher grade, deeper skarn section:

We’ve already seen JBY demonstrate that this might be the case in one hole, and there are existing diamond holes that haven’t been sampled in that section that could prove this theory even further:

We mentioned in our last note that there were results to come from one diamond drillhole that would be testing this theory.

Assays from that hole are still pending so we could get this news any day now.

With some re-sampling, and the results from that single hole we will know a lot more about this theory (hopefully soon).

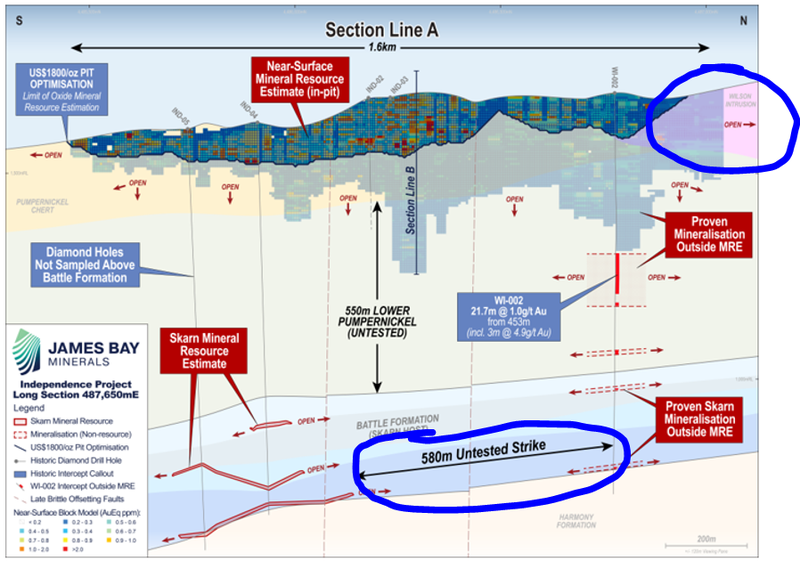

3. Extending drilling north and south

Third is the most obvious way - drilling extensions to the two resources north to south.

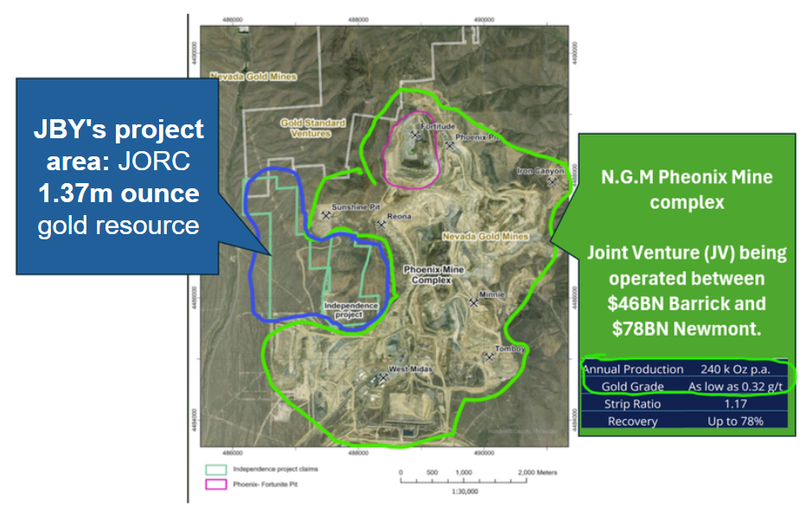

JBY is next door to Barrick and Newmont & now has the JV’s ex-geo...

JBY’s project is surrounded by existing gold mines in the “N.G.M Phoenix gold complex” - a Joint Venture (JV) being operated between two of the biggest gold mining majors going around - the $46BN Barrick and $78BN Newmont.

Nevada is also home to some of the lowest cost mines in the world.

Given that proximity to N.G.M we think the recent appointment by JBY is huge news.

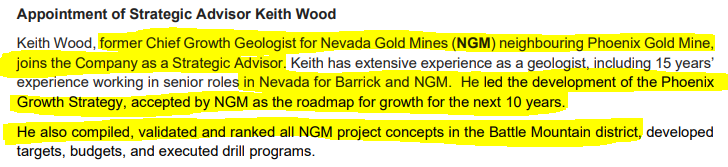

A few weeks ago JBY appointed Keith Wood as a “Strategic Advisor”.

Keith was the former Chief Growth Geologist for N.G.M and must have played a big role in the development of N.G.M’s growth strategy which is still in practice today...

We assume he would know the area extremely well, and will probably have a pretty good grip on what to do with JBY’s project...

We are especially interested in seeing what ideas he has for the shallow part of JBY’s resource.

The Barrick/Newmont JV is similar to that part of JBY’s project, producing ~240,000 oz of gold per year - from grades as low as 0.32g/t.

JBY’s JORC for the shallow part of its resource is ~395k ounces at similar grades.

JBY’s project also has a 2022 Preliminary Economic Assessment (PEA) which shows it could produce 32,050 ounces of gold per year for 6 years for US$1,078 per ounce. (source)

That study was done when gold prices were ~US$1,800 per ounce.

The gold price now is at ~US$2,900 per ounce.

With some exploration and Keith’s input we think the economics on this part of JBY’s project can improve pretty significantly on that 2022 PEA.

How today’s news impacts our JBY Investment Memo

After today’s news, JBY has completed objective #2 of our Investment Memo.

Objective #2: Convert foreign resource estimate into a JORC resource

We want to see JBY convert its existing foreign resource estimate into a JORC resource.

Milestones

✅ JORC conversion commenced

✅ JORC resource estimate completed

Source: “What do we expect JBY to deliver?” JBY Investment Memo 25 Nov 2024

We hoped the resource conversion wouldn't impact the resource too much.

Our base case expectation was to see the number fall slightly, this was one of the risks we flagged as part of our Investment Memo:

Resource risk [MITIGATED ✅]

Here’s what we wrote way back in November last year:

At the moment, JBY’s project has a “foreign resource estimate”. This means it is built on a different set of assumptions & guidelines relative to the JORC code that we are more accustomed to seeing on the ASX. There is no guarantee that JBY can convert all of its foreign resources into a JORC resource. If this risk were to materialise, it may have a negative impact on the company's share price.

Source: “What could go wrong” - JBY Investment Memo 25 Nov 2024

JBY’s upgrade of its foreign resource estimate to a JORC resource means that this risk is addressed, and objective #2 is completed for our Memo.

Click here to read our full JBY Investment Memo where you will find:

- What does JBY do?

- The macro theme for JBY

- Our JBY Big Bet

- What we want to see JBY achieve

- Why we are Invested in JBY

- The key risks to our Investment Thesis

- Our Investment Plan

[Reminder] 10 key reasons why we Invested in JBY:

Note the below was written in November 2024, you can read it here.

Where things have changed since November, we flag as an [UPDATE] below the reason.

1. JBY has a 1.18Moz gold and 7.6Moz silver resource with exploration upside.

JBY already has a foreign resource estimate of 1.18Moz gold, 7.6Moz silver. Inside this sits a 796Koz high-grade component (3.8Mt at 6.53g/t gold). The current resource is open at depth and in all directions with scope to upgrade that resource number. Right now, we think it is cheaper and lower risk to Invest in “already discovered” ounces in the ground - provided there is enough exploration upside at the project as well.

[UPDATE]

This reason is even more compelling - now that JBY has converted its resource into a JORC compliant estimate AND upgraded it to ~1.37M ounces of gold.

2. JBY has the same team and backers as our 2024 Small Cap Pick of the Year SS1.

Board, management, corporate advisor and top 20 shareholders are very similar across JBY and SS1 (our 2024 Small Cap Pick of the Year that IPOd at 20c and hit over $1.18 within nine months). We have observed them to be very hard workers and good holders so far - We are backing the same group to deliver a win with JBY. They also have a knack for securing quality, advanced projects on good deal terms, and maintaining good tight cap structures with no options overhang.

[UPDATE]

The team has been built out since November, with the recent board/management changes at JBY.

Founder of JBY (and SS1) Matt Hayes just came onboard as executive director.

Jay Ward (ex-Capricorn and Strickland Metals) has joined as exploration manager.

AND Keith Wood (ex-Nevada Gold Mines Chief Geologist) from the neighbouring Phoenix Mine JV between Barrick and Newmont has been appointed as a strategic advisor to the company.

3. We like the gold macro thematic for 2025 and beyond.

Gold is currently trading at all time highs and we think it will continue running. We are yet to see a wave of new production being brought online during this cycle, our expectations is that a lot more projects will get into production and start producing gold while spot prices are high. We are hoping JBY’s project is one that gets into production during this gold bull market window OR they build a resource big enough to be taken out by a bigger player in the region.

4. Nevada a top 3 Fraser Institute mining jurisdiction every year for the past 10 years.

Nevada was ranked as the best mining jurisdiction in the world in 2022 by the Fraser Institute. Nevada has also consistently ranked in the top 3 every year for the past 10 years.

5. We have success in Nevada in silver with SS1, JBY’s project is similar, but for gold.

Nevada is home to some of the biggest gold and silver mines in the world, including Barrick's “Goldstrike” project which was the asset that put the company on the map. The gold and silver deposits in Nevada are known for being easy to mine and process at a low cost. We have had success in Nevada with SS1, we are hoping that JBY can replicate this success.

6. JBY is right next door to a mine operated by Barrick and Newmont.

JBY’s project sits right in the middle of Barrick and Newmont’s Phoenix Joint Venture. Barrick and Newmont have sunk billions of dollars into mine infrastructure and are currently producing gold from the project. Barrick and Nemont have both committed to growing production at the Phoenix operation and there is always a chance that they look at a bolt on acquisition with a project like JBY .

7. JBY is surrounded by low cost heap leach mines with same geology

JBY’s project is surrounded by some of the lowest cost gold mining operations in the world. Barrick and Nemont’s Nevada Gold Mines JV has pits operating with AISC (all in sustaining cost) to produce at below ~US$1,000 per ounce. $19BN Kinross’ Bald Mountain asset operated with a cost of sales of ~US$1,241 per ounce in 2023. Great margins at the current spot price of ~US$2,700 per ounce.

8. Previous owners spent >US$25M on this project and have completed a Preliminary Economic Assessment (PEA)

JBY’s project has had over US$25M in capital spent to get the project to where it is today. The project also has a 2022 PEA which showed 32,050 ounces of gold per year for 6 years at an all-in sustaining cost of US$1,078 per ounce. By our calcs that is US$86M in revenues per year assuming a US$2,700 ounce gold price. That PEA only covered a small portion of JBY’s existing foreign resource, excluding the high grade skarn which contains a resource of 796Koz ounces of gold.

Note this rough calculation doesn’t take into account capex or opex etc and assumes a gold price that could move down (or up).

9. Clean, tight cap structure, ~89M shares post transaction, no options overhang

We like JBY’s capital structure because there are no option overhangs and only 89m shares on issue. We have seen a similar style clean structure for SS1 which has so far worked out well. A lot of the top 20 shareholders are the same across both companies and they appear to be stable long term holders so far. A clean structure with no options overhang allows for the company’s share price to rise off the back of strong positive news.

[UPDATE]

The capital structure remains very tight. Since the transaction, the main change to the capital structure was that the company raised $6M at 65c per share in December. JBY was trading below this share price at market close yesterday.

10. Well-known retail stock with potential to re-rate.

JBY appears to have a large retail following and the potential for share price re-rates on good news. The company promotes well, it was a hot IPO back in September of 2023, when James Bay lithium stocks were popular amongst investors and right before the lithium sentiment crash. As a result, we think that if the company can deliver material news on their gold project, there will be enough eyeballs on the stock for the share price to re-rate.

Our full JBY Investment Memo is at the end of this note, including objectives we want to see JBY achieve, risks we have identified and accepted and our Investment plan.

Our JBY Big Bet:

“JBY re-rates to a +$300M market cap by expanding its large US gold resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our JBY Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for JBY?

Assay results from the deeper diamond drilling 🔄

In the short term we want to see what comes of the deeper diamond drillhole JBY drilled beneath its existing resource:

Next round of drilling (starting this quarter) 🔄

JBY expects to kick off a drill program later this quarter.

As mentioned earlier, we are looking forward to JBY’s drill program because the company will test three different theories:

- Drilling out the shallow mineralisation currently outside of its resource model (and hopefully bringing it into the model in future resource updates).

- Drilling in between JBY’s two resources (shallow and deep sections)

- Drilling extensions to the north and south of the current JORC resource along strike.

What are the risks?

In the short term the key risk for our JBY Investment Thesis is exploration risk.

JBY still has assays pending from its last drill program AND plans to start drilling again later this quarter.

There is no guarantee that any of that drilling delivers any economically viable drill results.

If that were to happen we would expect the market to react negatively and move the JBY share price lower.

Exploration risk

There is no guarantee that JBY can increase its existing resource estimate through exploration drilling. There is always a chance that drill programs fail to find any economic mineralisation that may not add to the project’s overall resource estimate.

Source: “What could go wrong” - JBY Investment Memo 25 November 2024

To see other risks to our Investment Thesis, check out our JBY Investment Memo here.

Our JBY Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our JBY Investment Memo where you will find:

- What does JBY do?

- The macro theme for JBY

- Our JBY Big Bet

- What we want to see JBY achieve

- Why we are Invested in JBY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.